A senior underwriter at a mid-sized Australian carrier spends the first hour of every working day doing triage. New submissions from brokers. Missing documents. Wrong-queue routing. Loss runs that need parsing before anyone can form a view. That is not underwriting. That is sorting.

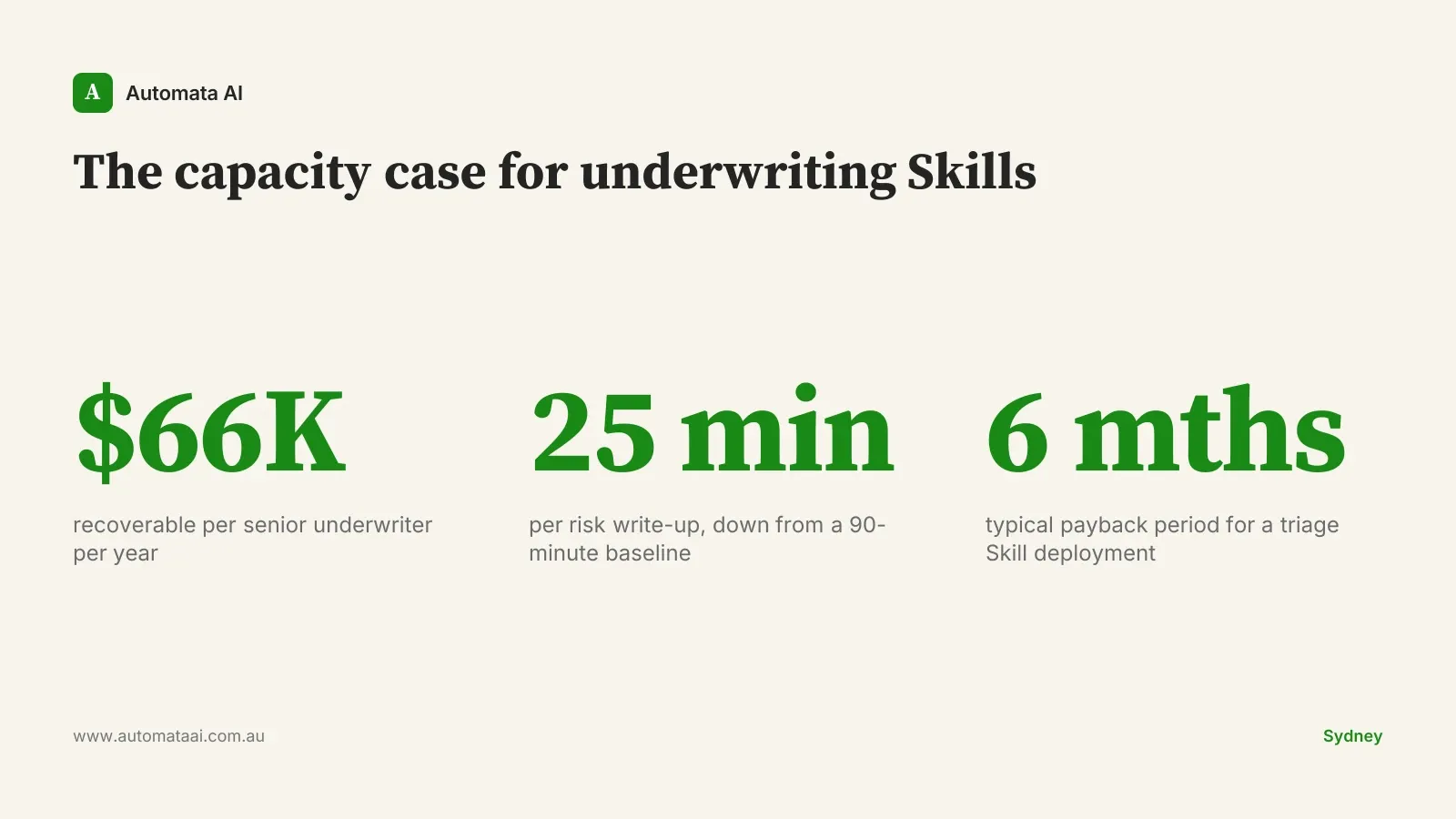

At a fully loaded rate of $230,000 per year, that daily sorting hour costs roughly $28 per minute. For a carrier with 25 underwriters each absorbing 12 hours per week on triage, write-ups, and compliance prep, the recoverable capacity exceeds $1.6 million per year. That is $66,000 per underwriter. It is not speculative. It comes from mapping the three workflows below against an underwriter's hourly rate.

Run the payback model against your own headcount in the ROI Calculator. AUD figures, three minutes, no signup required.

The three workflows worth automating first

Not everything in an insurance underwriting shop is automatable. The judgement call on a complex risk, the negotiation of terms, the broker relationship. Those stay with the underwriter. The three workflows below are different. They are high-volume, rule-bound, and currently absorbing senior capacity that should be going to decisions. The issue is not capability. Most carriers already have documented underwriting guidelines detailed enough to train a Skill. The issue is that nobody has connected those guidelines to the right tool. That gap is smaller than it looks.

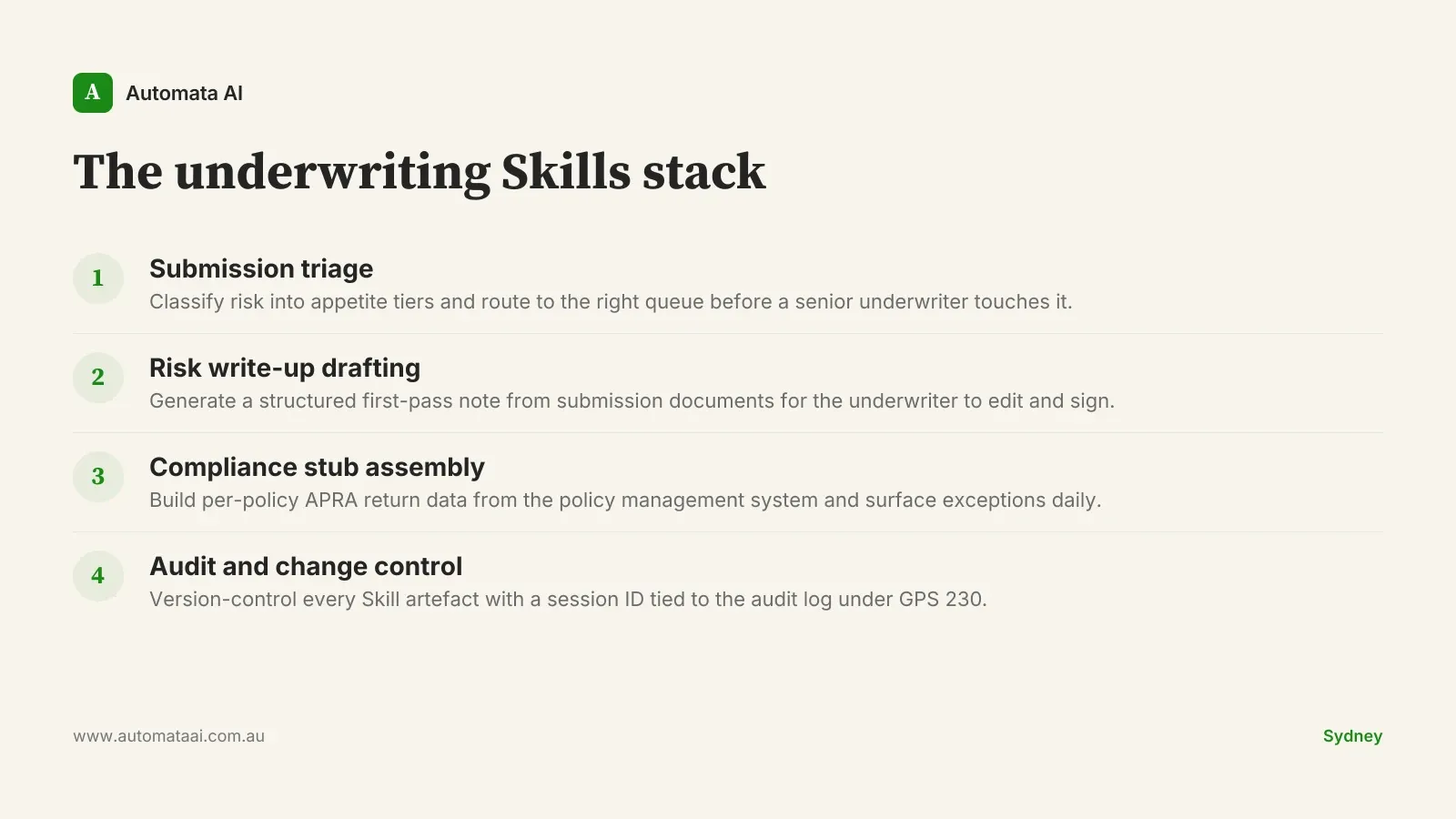

Skill 1: Submission triage

A new submission arrives from a broker. The Skill reads the submission summary and supporting documents, classifies the risk against the carrier's appetite guide, and routes it to the right underwriter queue. The whole sequence runs before a senior underwriter sees the item.

Appetite tier classification. The Skill returns in-appetite, marginal, or declined-by-policy, with a short reasoning note tied to the carrier's underwriting guide.

Queue and underwriter routing. The Skill recommends a queue based on industry class and limit size, matched to each underwriter's specialisation.

Document completeness flag. Any submission missing required attachments is flagged before it enters the queue, so underwriters are not chasing brokers mid-review.

Most carriers implementing the triage Skill recover 45 to 60 minutes per underwriter per day. Senior underwriters start the morning at the top of a prioritised queue, not at the bottom of an inbox. Across a 25-person book, that is over 100 hours of recovered senior capacity per week.

Skill 2: Risk write-up drafting

For risks the carrier wants to quote, the underwriter writes a risk note covering the business, the loss history, the exposures, and the rationale for the premium. The typical write-up takes 60 to 90 minutes. A drafting Skill reduces that to around 25 minutes.

Business description. Pulled from the submission and cross-referenced with ASIC company records, including ABN, industry classification, and registered address.

Loss history summary. Five years of prior losses with severity tags: attritional, large loss, or catastrophe exposure.

Exposure schedule. Mapped against the carrier's standard template, with gaps flagged for the underwriter to fill.

Rationale paragraph. Anchored to the section of the carrier's underwriting guide that governs this risk class.

The underwriter reads it, corrects anything wrong, and signs. The Skill does not underwrite. It drafts. That distinction matters for governance and for the APRA audit trail.

Skill 3: Compliance stub assembly

APRA returns and other regulatory submissions require structured per-policy data extracts from the underwriting book. A Skill builds those stubs daily from the policy management system, applies the correct APRA classification, and queues them for the compliance team's review.

This is not glamorous work. It is auditable work. Running the extraction daily means exceptions surface when there is still time to correct them. End-of-period scramble shrinks to a final review of a pre-assembled queue rather than a 48-hour data sprint.

Together, these three workflows form what we call the underwriting Skills stack: triage, write-up drafting, and compliance stub assembly. Most carriers can deploy all three without replacing their policy management system or rewriting their underwriting guidelines. The stack sits on top of the existing workflow, not in place of it. For a carrier with mature documentation and submission volume above 100 per month, all three Skills can be live in under eight weeks.

When Skills do not belong in the underwriting workflow

Three circumstances where the economics or the governance do not support a Skill deployment:

The process is undocumented. If your appetite guide lives inside three senior underwriters' heads rather than in a written document, the Skill has nothing to anchor to. Document the guidelines first. The Skill is a downstream step.

Submission volume is under 50 per month. Below that threshold, a $30,000 to $60,000 build cost will not recover quickly. The capacity case requires volume to close.

The regulatory obligation is in flux. A Skill built for GPS 230 reporting during an APRA consultation period needs rewriting every quarter as the standard evolves. Wait until the obligation stabilises.

Governance for APRA-regulated carriers

APRA GPS 230 and CPS 234 treat material operational processes as controls subject to documentation, testing, and change management. A Skill deployed in an underwriting workflow is a material control. For the broader regulatory context covering AI deployments across the sector, our Australian financial services automation guide goes into the prudential standards in detail.

In practice, each Skill artefact is version-controlled and signed off by a senior underwriter and the compliance officer. Updates go through change control tied to the underwriting guidelines. Every output carries a session ID that connects back to the audit log. If an underwriting decision is ever challenged, the trail runs from the output to the Skill version to the guideline revision to the sign-off record. That is what makes the regulator's first question after an incident answerable, not the question that stalls the entire program.

If your carrier is sizing a Skills deployment, the AI Readiness Assessment maps your current workflow state against what a production deployment requires.

Pick one workflow. The triage Skill is usually the fastest to build and the easiest to justify internally. Map the current time cost per underwriter, multiply by headcount, and model the payback. For most carriers above 15 underwriters, the business case closes in under six months. If you are not sure where the time is actually going, that is the first thing to measure.