Your Microsoft rep has probably already called. The OpenAI-Microsoft partnership update landed last month, and if your organisation runs a Microsoft-heavy stack, you will be told this changes everything.

It does not change everything. Some of it does matter. Here is what is real.

What the partnership update covers

Microsoft and OpenAI restructured the commercial terms governing how OpenAI models distribute through Microsoft surfaces. Four concrete elements came out of the announcement.

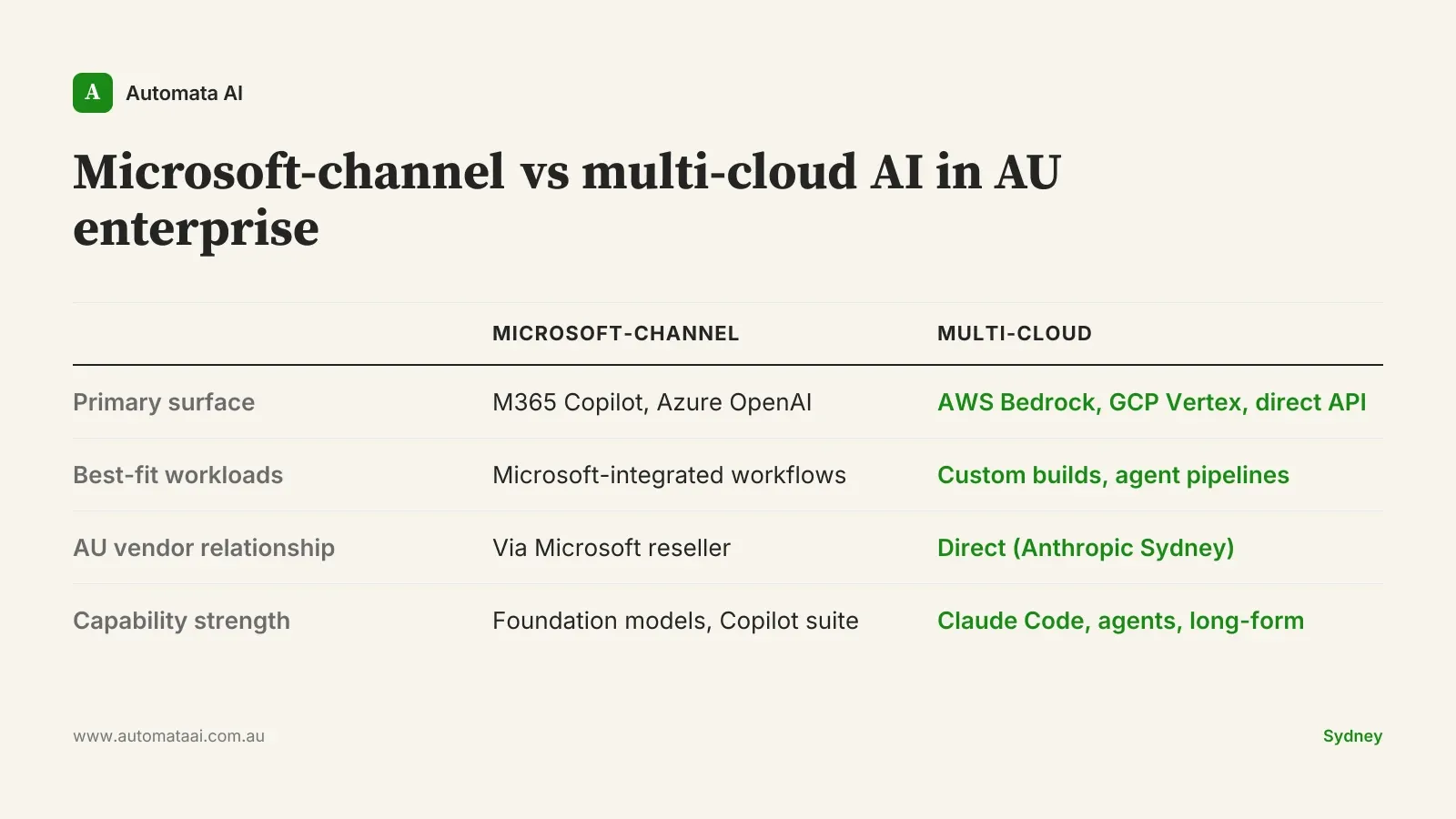

Continued distribution through Copilot and Azure. OpenAI models remain the engine behind Microsoft 365 Copilot and Azure OpenAI Service. No change in access for Australian enterprises on either surface.

Updated commercial terms between both companies. The financial arrangement was restructured to reduce OpenAI's dependency on a single large customer. Commercial stability for both parties.

Continued Microsoft compute access for OpenAI. Microsoft's infrastructure underpins OpenAI's training and serving capacity. That relationship continues without interruption.

Clarified scope for OpenAI's independent surfaces. ChatGPT, the OpenAI API, and direct enterprise sales remain OpenAI's own distribution, not absorbed into the Microsoft channel.

Four implications for Australian enterprise buyers

For Australian enterprises with meaningful Microsoft AI commitments, particularly those in financial services, professional services, and government, four things are now clearer.

1. Copilot rollouts planned for 2026 are stable

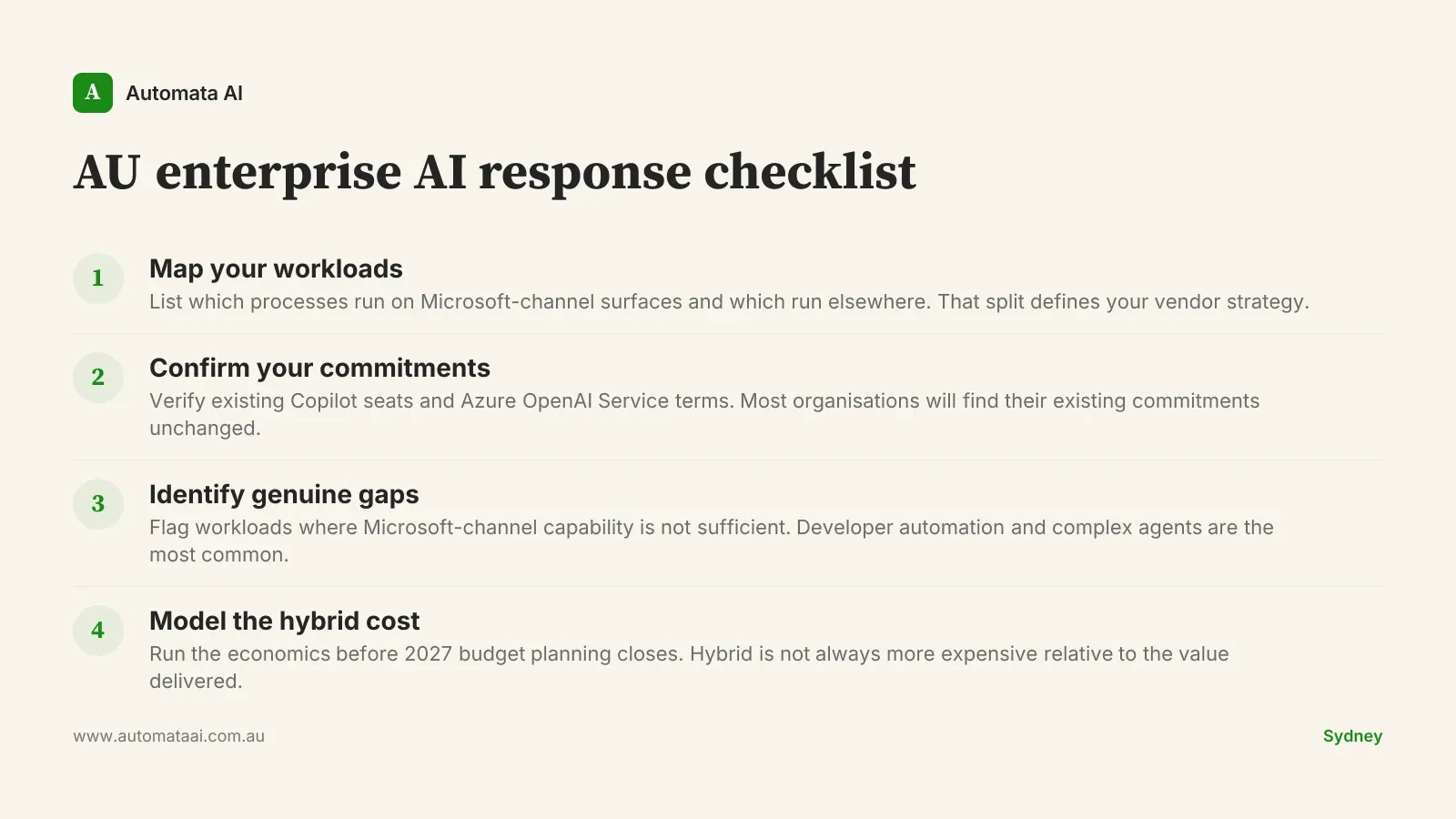

Australian enterprises that committed to Microsoft 365 Copilot rollouts this year can proceed without vendor-stability concerns. If your organisation was waiting on certainty before expanding from a pilot cohort to the broader business, you now have it. The relationship is durable, and the updated terms give both Microsoft and OpenAI clearer commercial footing going into 2027 contract cycles.

2. Azure OpenAI Service has solid footing

AU enterprises running Azure-native AI workloads (document processing, retrieval-augmented pipelines, internal knowledge search) are on stable ground. For Australian financial services firms with APRA CPS 230 operational resilience requirements that include third-party AI vendor review, the explicit preservation of the compute and model-access arrangement is a relevant data point for your next vendor risk assessment. No migration risk, and no reason to plan for one.

3. Compute risk is off the vendor risk list

One concern that surfaces in Australian vendor risk discussions: what if OpenAI degrades service quality because it cannot source enough compute? Microsoft's continued infrastructure commitment takes that question off the table. You can close that line item in your next vendor risk review.

4. Microsoft-channel pricing stays competitive

Microsoft has been aggressive on Copilot bundling, particularly for organisations already at M365 E3 or E5 licensing tiers. The strengthened partnership gives Microsoft further incentive to keep Copilot pricing competitive through 2026. Expect that posture to hold into your next renewal cycle.

When this announcement should not drive your decisions

If your AI footprint is a handful of Copilot licences that came with an M365 E3 renewal, this announcement has no operational significance for you. Do not let a vendor press release set your AI roadmap.

The organisations this matters for are those with material Azure OpenAI Service deployments, multi-year Copilot commitments at scale, or active procurement conversations where vendor stability was a documented blocker. Everyone else should return to their own workload prioritisation. Buy the tools that solve the problems you have already identified. The partnership update confirms existing direction. It does not create new direction.

Where this leaves Claude in the AU enterprise picture

Claude's positioning in the Australian enterprise market has not shifted because of this announcement. Three structural advantages remain worth naming explicitly, because they tend to get lost when Microsoft-OpenAI news dominates the vendor conversation.

Multi-cloud distribution. Claude runs on AWS Bedrock, Google Cloud Vertex AI, and direct API. For Australian financial services and government organisations with multi-cloud infrastructure requirements, often driven by APRA CPS 230 operational resilience obligations, this matters structurally, not just commercially.

Direct vendor relationship. Anthropic's commercial relationship with Australian enterprise customers is direct, reinforced by the Sydney presence established in 2025. That is a different dynamic from accessing OpenAI through a Microsoft reseller arrangement.

Workload-specific capability advantages. Claude leads in developer automation via Claude Code, complex agentic task execution, and long-form document analysis. These are not workloads where Microsoft-channel OpenAI is the natural fit.

The honest framing: most large Australian enterprises will end up running both vendors. That is not hedging. It is the correct technical answer when workloads split across Microsoft-native and multi-cloud surfaces.

Practical response by stack type

The right move depends on your actual environment.

Microsoft-native enterprises. Continue your Copilot rollout. Expect continued product investment from both Microsoft and OpenAI through 2026. Add Claude specifically where capability gaps exist (developer automation, complex agent workflows), rather than as a generic diversification move.

Multi-cloud enterprises. Maintain Claude as your primary custom-build AI surface. Use Microsoft-channel OpenAI where it fits Microsoft-integrated workflows. Do not replace one with the other, and do not let this announcement prompt a redundant evaluation cycle.

Mixed enterprises. A hybrid posture is operationally reasonable. For a 300-staff AU mid-market organisation covering both stacks, expect $400,000 to $900,000 annually in AI spend, covering licences, integration, and ongoing support at appropriate depth.

The cost math for AU enterprise

The three-year cost picture for a mid-market AU enterprise running both vendors sits at $1.2M to $3M total, depending on user count, custom development depth, and support structure. Single-vendor commitments at the same scale run 30 to 50 percent lower, but accept narrower workload coverage.

That premium is justifiable when your workloads genuinely split across both surfaces. It is not justifiable when you are paying for a second vendor as an insurance policy you never intend to claim. Insurance you do not use is not a strategy. It is budget leakage.

Your 2027 AI budget conversations are probably starting now. The vendor stability question has been answered. The workload mapping question has not. That is the one worth spending time on.