Month-end close is the job nobody puts on the calendar but everyone dreads. For a lot of Australian small businesses, the last week of the month disappears into bank reconciliations, chasing missing receipts, and squinting at a profit-and-loss report that does not quite add up. Claude will not replace your bookkeeper or your accountant, but it can take the repetitive reading, matching, and drafting off their plate so the close takes days instead of a fortnight.

This is a walkthrough of how a real close works with Claude in the loop, based on the pattern we set up for Sydney and Melbourne clients. The point is not to automate judgement. It is to remove the manual grind around the judgement so the people who own the numbers spend their time on the parts that actually need a brain.

What a month-end close actually involves

Before you can decide where Claude helps, it is worth naming the work. A typical close for a business turning over a few million dollars a year runs through the same checklist every month:

Reconciling every bank and card account against the accounting ledger in Xero or MYOB

Categorising transactions that came in without a clear description

Matching supplier invoices to bills and flagging anything paid twice

Reviewing the GST coding so the quarterly BAS is not a last-minute scramble

Posting accruals and prepayments so the month reflects what really happened

Writing a short commentary on why revenue or margin moved

Most of that list is reading and matching. A smaller part is genuine accounting judgement. The trick is separating the two, because Claude is very good at the first and should never be trusted alone with the second.

Where Claude fits, and where it does not

Claude is a strong reader and a careful drafter. Give it a bank statement export and the ledger, and it will tell you which lines do not match and suggest a category for each orphan transaction. Give it twelve months of history and it will spot that your $4,200 software renewal was coded to three different accounts across the year. What it will not do is decide whether a payment is a capital expense or a repair. That is a call your accountant makes, and it carries real tax consequences.

Good jobs to hand Claude

Drafting categories for uncoded transactions, with a plain reason for each one

Cross-checking supplier bills against the payments run to catch duplicates

Turning a raw profit-and-loss export into a plain-English variance note

Building the month-end checklist and tracking what is done

Jobs to keep with a human

Final GST treatment and anything that changes the BAS lodged with the ATO

Capital versus expense decisions

Signing off the numbers that go to the bank, the board, or the owner

A realistic walkthrough

Here is how a close ran last month for a wholesale client with about $6 million in annual revenue and roughly 900 transactions a month. Their bookkeeper used to spend three full days on it. With Claude handling the reading, it now takes one.

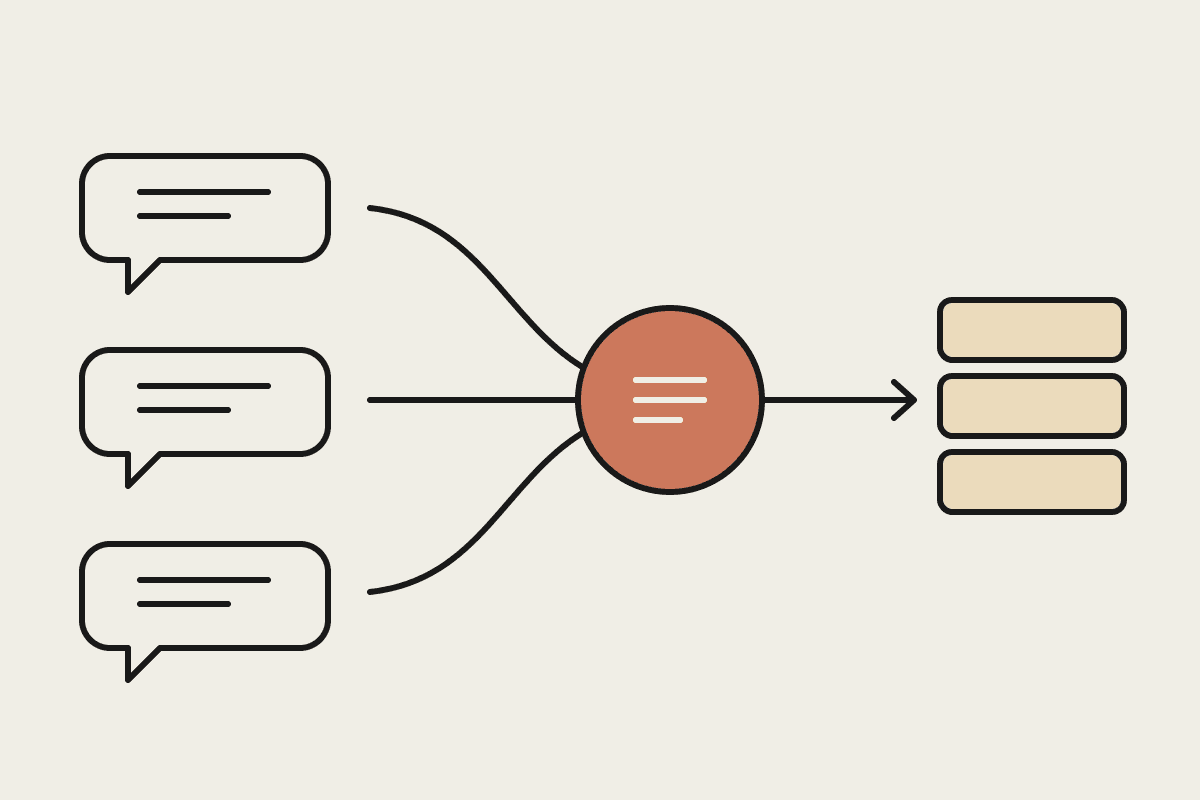

Step one, reconcile. The bookkeeper exports the bank feed and the Xero ledger as CSV files and hands both to Claude. Claude matches them line by line and returns a short list of the forty or so transactions that do not reconcile, grouped by likely cause. No money moves and no transaction leaves the business; the files stay on the bookkeeper's own machine.

Step two, categorise. For each unmatched line, Claude proposes a category and explains why, referencing how similar transactions were coded before. The bookkeeper accepts most in a couple of minutes and overrides the handful that need a real decision.

Step three, check for duplicates. Claude compares the supplier bills against the payments run and flags a $3,800 invoice that looks like it was paid twice. It was. That single catch covered the cost of the whole setup for the quarter.

Step four, write the commentary. Claude takes the finished profit-and-loss and drafts a half-page note: revenue up 9 percent on strong June orders, gross margin down two points because freight rose, one large legal bill that will not recur. The accountant edits it and sends it to the owner the same afternoon.

What it costs and what you save

The maths is not complicated. That bookkeeper was spending roughly 24 hours a month on the close. Cutting it to eight hours frees 16 hours, which at a loaded cost of around $65 an hour is about $1,040 a month, or $12,500 a year. Set against a Claude subscription of a few hundred dollars a year plus a one-off setup, the payback is measured in weeks, not years. The duplicate bills and coding errors it catches sit on top of that.

The bigger win is timing. When the close drops from a fortnight to a few days, the owner sees the real numbers while they can still act on them. A cash problem spotted on the 5th is a very different thing from the same problem spotted on the 20th.

Keeping it safe and compliant

Financial data is sensitive, so the setup matters. We keep exports on the business's own machines and hand Claude only what a given task needs, not the whole ledger with customer details attached. Under the Privacy Act, personal information in your books still has to be handled properly, so we strip names and account numbers where they are not needed for the task. Claude is used to read and draft, and a person always approves anything that changes the accounts or the BAS.

None of this asks you to trust a machine with your books. It asks the machine to do the reading so your bookkeeper and accountant can do the thinking. If you want to see what a month-end close looks like with Claude in the loop for your business, book a short call and we will map it against your actual process.